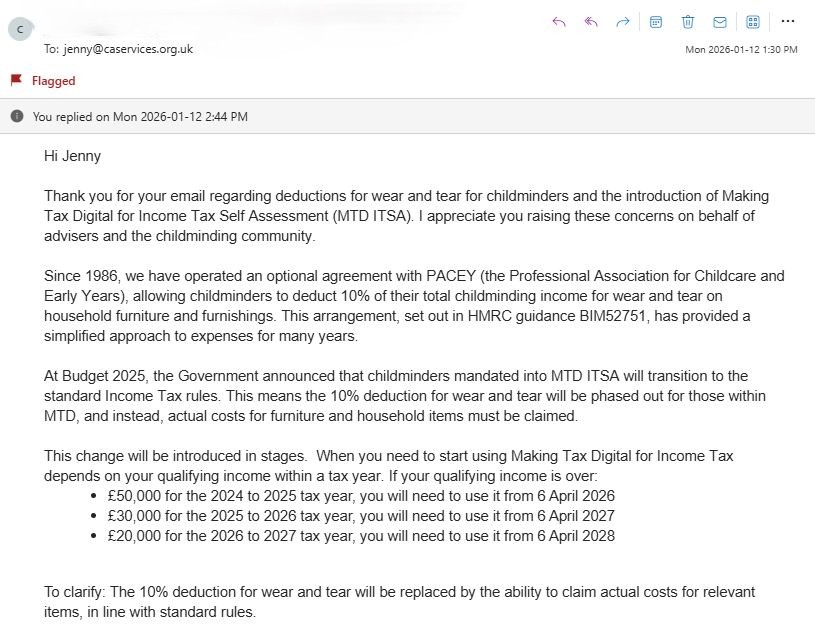

There has been a lot of confusion recently in the childminding community regarding the long-standing 10% wear and tear deduction, and what will happen to it once Making Tax Digital for Income Tax Self Assessment (MTD ITSA) is introduced. To help remove uncertainty, we contacted HMRC and have now received confirmation directly from the HMRC Making Tax Digital Director. This blog explains what HMRC have confirmed, when it will affect you, and what you may need to do next.

The current 10% wear and tear deduction (PACEY agreement)

For many years, childminders have been able to use an optional simplified approach to claim wear and tear on household furniture and furnishings, instead of claiming actual costs. This is the well-known 10% wear and tear deduction, which has been available under an agreement with PACEY. Many childminders have relied on this method because it is simple and avoids the need to track and justify individual household items.

What HMRC have now confirmed

HMRC have confirmed that childminders mandated into MTD ITSA will move onto the standard Income Tax rules. This means that the 10% wear and tear deduction will be phased out for those within MTD, and instead childminders will need to claim actual costs for relevant items, following the normal rules. In other words, once you are brought into MTD ITSA, the flat-rate 10% wear and tear method will no longer apply, and you will claim expenses using actual expenditure going forward.

When does MTD ITSA start?

MTD ITSA is being introduced in stages and the start date depends on your qualifying income in a tax year. HMRC have confirmed the thresholds and start dates as:

- Over £50,000 (2024 to 2025 tax year) – MTD ITSA will start from 6 April 2026

- Over £30,000 (2025 to 2026 tax year) – MTD ITSA will start from 6 April 2027

- Over £20,000 (2026 to 2027 tax year) – MTD ITSA will start from 6 April 2028

What does “claiming actual costs” mean for childminders?

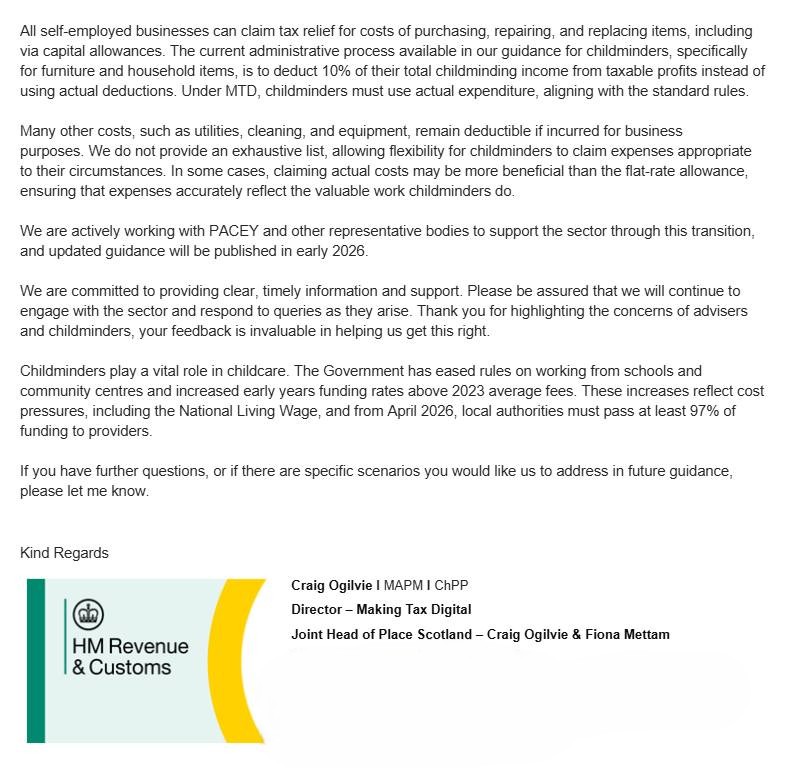

Under the standard rules, the expectation is that self-employed businesses claim tax relief based on allowable costs incurred for the business. This means that childminders will need to claim actual costs for relevant household furniture and items that are used for childminding, rather than relying on the 10% deduction. Other costs such as utilities, cleaning and equipment continue to be claimable where they are incurred for the business. Every childminding setting is different, so claims will always depend on individual circumstances.

A note on cash basis

Cash basis is now the default method for many sole traders, and a large number of childminders will be using cash basis. Because cash basis can affect how certain costs are treated, we have asked HMRC for further guidance and clarity specifically on the cash basis position, to ensure childminders understand what they can and cannot claim once the 10% method is removed. We will share a further update as soon as HMRC provide additional guidance on this point.

HMRC confirmation (screenshot)

We are sharing a screenshot of the confirmation email below, with HMRC’s permission. All contact details have been removed.